The UK is not entering 2026 in crisis. But it is entering it weaker than it looks.

Behind the surface-level stability — steady employment, controlled inflation, familiar rhetoric — the private sector is stepping back. Investment decisions are being delayed. Hiring intentions are softening. Confidence is thinning.

This matters because long-term economic power in the UK does not sit with the state. It sits with firms willing to deploy capital, build capacity, and take risk. When that engine slows, the consequences are uneven — and the North feels them first.

What Just Happened

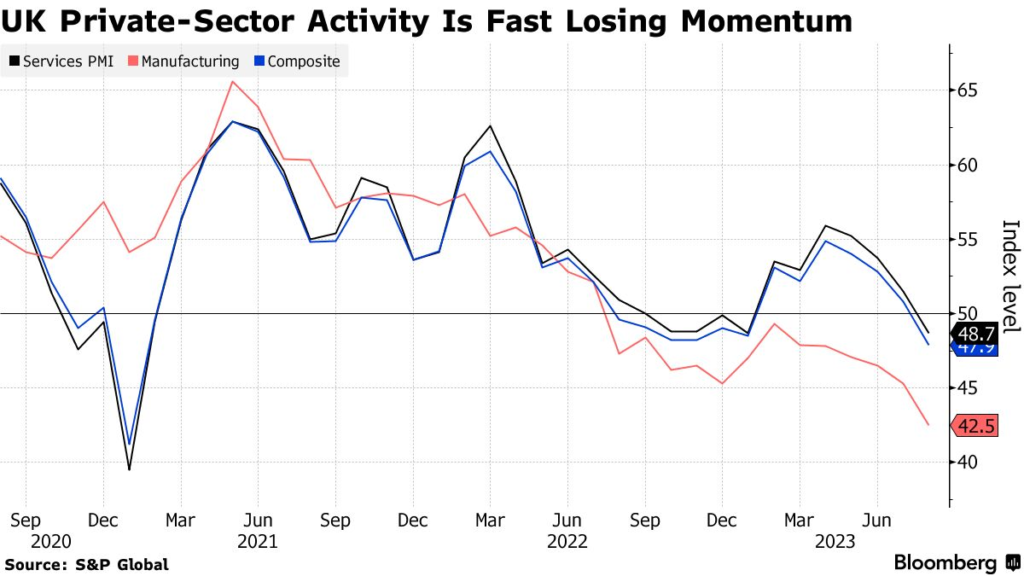

According to business surveys from the Confederation of British Industry, private-sector output is contracting sharply as the UK heads into 2026. Firms across services and manufacturing report falling order books, weak demand, and little appetite for expansion.

This is not a sudden shock. It is the result of prolonged uncertainty, elevated borrowing costs, fragile productivity, and a policy environment that has failed to give businesses a clear growth horizon Untitled document.

In practical terms: businesses are choosing resilience over ambition.

Why This Matters for the North

The North’s economic recovery over the last decade has relied on one fragile assumption — that private capital would increasingly see regional growth as investable, not charitable.

A private-sector downturn tests that assumption.

When confidence dips, capital does not retreat evenly. It clusters around perceived certainty:

large firms, central markets, established balance sheets.

For the North, this creates four immediate risks:

- Delayed industrial investment, especially in advanced manufacturing and energy-adjacent sectors.

- Stalled scale-ups, as growth capital becomes more selective and risk-averse.

- Weakened local institutions, forced to bridge gaps with short-term funding rather than long-term strategy.

- Erosion of ownership, as regional assets struggle to access patient capital and drift toward extractive control.

This is how regional inequality reproduces itself — quietly, structurally, and without headlines.

Second-Order Effects

If this private-sector pullback continues, pressure will compound:

- Supply chains tighten as smaller firms struggle with cash flow.

- Productivity gains stall as capital expenditure is postponed.

- Skills pipelines weaken as firms reduce training and long-term workforce planning.

But there is also a counter-signal.

Periods like this reward regions that have done the institutional work in advance:

clear governance, aligned stakeholders, credible investment frameworks.

Capital doesn’t vanish in downturns. It demands better reasons to stay.

What Should Happen Next

This moment does not call for louder policy announcements. It calls for institutional maturity.

Regional leaders should prioritise fewer, stronger bets — projects with clear industrial logic and long-term ownership structures.

Investors should look beyond national averages and identify places where coordination already exists between councils, universities, anchor employers, and capital.

National institutions should recognise that resilience is now a regional trait — and that supporting it requires mechanisms, not slogans.

The real deficit is not confidence. It is architecture.

Long-Horizon Signal

Over the next 10–20 years, the UK economy will not be reshaped by short cycles of growth and contraction. It will be shaped by where private capital feels safe committing for decades.

A private-sector slowdown exposes the truth:

regions without durable institutions are passengers.

Regions that build them become anchors.

The North’s future will not be decided by whether growth returns — but by whether it is structurally ready when it does.

Leave a Reply